Unlocking The PPP Loan List Of Names: A Comprehensive Guide

The Paycheck Protection Program (PPP) served as a critical lifeline for countless businesses, providing necessary financial support amidst economic turmoil. As businesses scrambled to secure funds, the PPP loan list of names became a key point of interest for many individuals seeking transparency and accountability. The list not only sheds light on the distribution of funds but also provides insights into the businesses that benefited from the program. Though the PPP loans were pivotal in sustaining businesses during challenging times, understanding who received these loans remains a topic of curiosity and scrutiny.

In this comprehensive guide, we will delve into the significance of the PPP loan list of names, exploring its implications for businesses, the economy, and the public. We'll navigate through the intricacies of the PPP, from the criteria for loan eligibility to the process of loan forgiveness. Our exploration will also include a detailed examination of the controversies surrounding the list and its impact on public perception. By the end of this article, you'll have a well-rounded understanding of the PPP loan list of names, equipped with insights that underscore its importance in the broader economic landscape.

Whether you're a business owner, a policy analyst, or simply a curious reader, this guide is designed to provide a thorough understanding of the PPP loan list of names. We aim to offer clarity on the complex narrative surrounding the list, while also addressing frequently asked questions to enhance your comprehension. Let's embark on this informative journey together, unraveling the layers of the PPP loan list of names with an optimistic lens on its potential to inform and educate.

- Understanding PPP Loans

- Eligibility and Application Process

- Importance of the PPP Loan List

- How the PPP Loan List Was Compiled

- Transparency and Accountability

- Controversies Surrounding the PPP Loan List

- Economic Impact

- Case Studies of PPP Loan Recipients

- Legal and Ethical Considerations

- Loan Forgiveness Process

- Future of Small Business Loans

- Frequently Asked Questions

- Conclusion

Understanding PPP Loans

The Paycheck Protection Program (PPP) was established under the Coronavirus Aid, Relief, and Economic Security (CARES) Act. Its primary goal was to provide financial assistance to small businesses, enabling them to maintain their payroll and cover other operational costs during the COVID-19 pandemic. This section will explore the foundational aspects of PPP loans, including their objectives, structure, and the pivotal role they played in stabilizing the economy during unprecedented times.

PPP loans were essentially forgivable loans provided by the Small Business Administration (SBA) to help businesses keep their workforce employed. The program was designed to prioritize small businesses, which are often hit hardest during economic downturns. The loans could be used for payroll costs, rent, utilities, and mortgage interest, among other expenses. A key feature of the PPP was its forgiveness aspect, which allowed businesses to have their loans forgiven if they adhered to certain criteria, such as maintaining workforce numbers and using the funds for eligible expenses.

The introduction of PPP loans marked a significant intervention by the federal government, aiming to curb the economic fallout from the pandemic. The program was rolled out in phases, with various legislative updates and funding rounds to accommodate the evolving needs of businesses. As a result, the PPP became one of the largest financial aid programs in U.S. history, distributing billions of dollars to businesses across the country.

Eligibility and Application Process

Understanding the eligibility criteria and application process for PPP loans is crucial for comprehending the broader context of the PPP loan list of names. This section will delve into the specifics of who qualified for these loans and the steps involved in securing them.

To qualify for a PPP loan, businesses had to meet specific criteria established by the SBA. These criteria included being a small business with 500 or fewer employees, a sole proprietorship, an independent contractor, or a self-employed individual. Certain non-profit organizations, veterans organizations, and tribal businesses were also eligible. Additionally, businesses had to demonstrate that the loan was necessary to support their ongoing operations due to the uncertainty of current economic conditions.

The application process for PPP loans was streamlined to facilitate quick access to funds. Businesses applied through approved lenders, which included traditional banks, credit unions, and online lenders. The application required basic information about the business, including payroll costs, number of employees, and the intended use of the loan. Lenders were tasked with processing applications and disbursing funds, with guidance and oversight from the SBA.

The demand for PPP loans was immense, with businesses rushing to secure funds before they were exhausted. As such, the application process was not without challenges, as many businesses faced delays and navigated complex bureaucratic requirements to obtain their loans.

Importance of the PPP Loan List

The PPP loan list of names serves as a vital tool for transparency and accountability. By revealing the recipients of these loans, the list provides insights into how federal funds were distributed and highlights the businesses that were deemed essential for economic recovery.

The importance of the PPP loan list extends beyond mere transparency. It allows stakeholders, including policymakers, researchers, and the public, to analyze trends in the allocation of funds. This analysis can inform future policy decisions and ensure that financial aid programs effectively target businesses in need. Moreover, the list can help identify potential disparities in the distribution of loans, prompting discussions about equity and fairness in government aid programs.

For businesses, being included on the PPP loan list can carry significant implications. While many businesses benefited from the support, the public disclosure of loan recipients also subjected them to scrutiny. This scrutiny was particularly pronounced for larger companies or those with substantial financial reserves, raising questions about the criteria used to determine eligibility and the ethical considerations of accepting government aid.

How the PPP Loan List Was Compiled

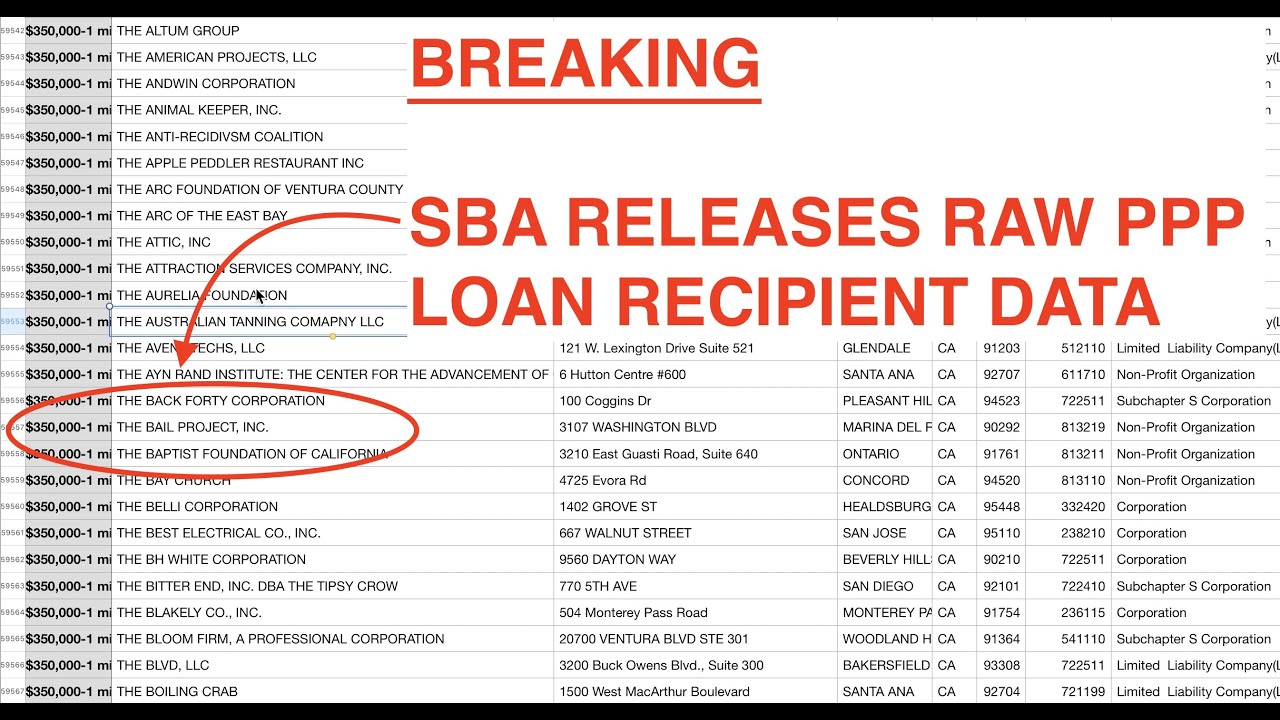

The compilation of the PPP loan list involved a complex process of data collection, verification, and publication. This section will explore the mechanisms through which the list was created, highlighting the role of the SBA and other stakeholders in ensuring its accuracy and reliability.

The SBA was primarily responsible for collecting data on PPP loan recipients. Lenders submitted information on approved loans, including the names of businesses, loan amounts, and the number of jobs supported. This data was then aggregated and reviewed by the SBA to ensure compliance with program guidelines.

To promote transparency, the SBA made the decision to publicly disclose the names of businesses that received loans over $150,000. This disclosure included additional details such as the business type, industry, and location. For loans under $150,000, the SBA provided aggregate data without specific business names, balancing transparency with privacy considerations for smaller businesses.

The publication of the PPP loan list was met with both praise and criticism. While many lauded the SBA's efforts to foster transparency, others raised concerns about potential inaccuracies or omissions in the data. The SBA worked to address these concerns by updating the list periodically and providing channels for businesses to report errors or discrepancies.

Transparency and Accountability

Transparency and accountability are central themes in the discussion of the PPP loan list of names. By publicly disclosing the recipients of loans, the SBA aimed to ensure that the program operated with integrity and that funds were allocated to deserving businesses.

The decision to release the PPP loan list was driven by a desire to foster public trust in the program. In doing so, the SBA sought to demonstrate that federal funds were being used responsibly and that businesses were adhering to the terms of their loans. The list also served as a deterrent against potential fraud or misuse of funds, as businesses were aware that their participation in the program was subject to public scrutiny.

Accountability measures extended beyond the publication of the list. The SBA implemented rigorous auditing processes to verify the legitimacy of loans and ensure compliance with program guidelines. Businesses found to have misrepresented their eligibility or used funds inappropriately faced penalties, including the possibility of having their loans converted to repayable debt.

The emphasis on transparency and accountability underscored the federal government's commitment to safeguarding taxpayer dollars and supporting the economic recovery of businesses most in need.

Controversies Surrounding the PPP Loan List

The release of the PPP loan list was not without controversy. Several high-profile incidents and criticisms emerged, sparking debates about the program's efficacy and fairness.

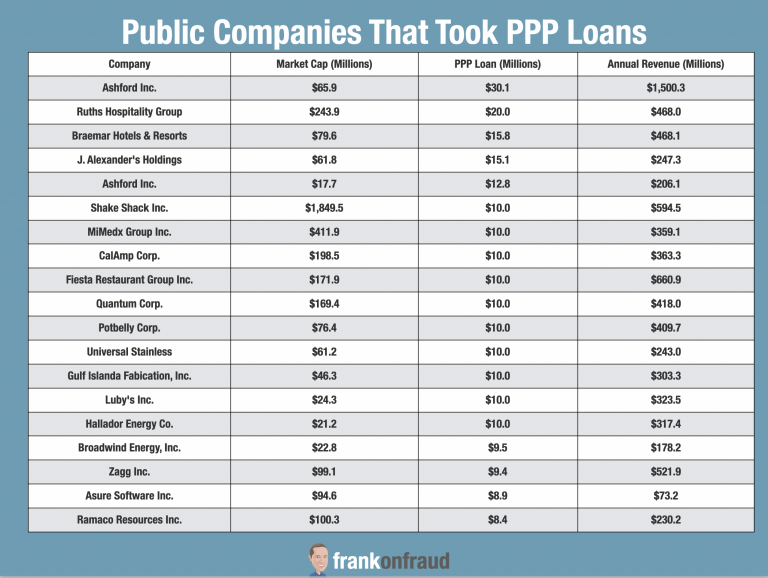

One major controversy centered around the inclusion of large corporations and publicly traded companies on the list. Critics argued that these entities had access to other sources of capital and should not have received PPP loans intended for small businesses. In response, some companies opted to return their loans amid public backlash.

Another point of contention was the perceived inequity in the distribution of funds. Reports surfaced of minority-owned and women-owned businesses facing greater challenges in securing loans, leading to accusations of systemic bias in the lending process. This prompted calls for reforms to ensure that future aid programs prioritize underserved communities.

The accuracy of the PPP loan list also came under scrutiny, with some businesses claiming they were incorrectly listed or that their loan amounts were misreported. The SBA worked to address these concerns by updating the list and providing mechanisms for businesses to correct errors.

Despite these controversies, the PPP loan list remains a valuable resource for understanding the program's impact and guiding future improvements in government aid initiatives.

Economic Impact

The economic impact of PPP loans and the accompanying loan list is profound, influencing businesses, employment rates, and the broader economic landscape. This section will explore the tangible effects of the program and the insights gained from analyzing the loan list.

PPP loans played a crucial role in stabilizing the economy during a period of unprecedented uncertainty. By providing financial support to businesses, the program helped avert widespread layoffs and business closures. This, in turn, had a positive impact on employment rates and consumer spending, contributing to a more stable economic environment.

The PPP loan list offers valuable data for assessing the program's effectiveness in achieving these outcomes. By examining the distribution of loans across industries and regions, policymakers and researchers can identify trends and areas where additional support may be needed. This analysis can inform future economic recovery efforts and ensure that aid is targeted where it is most impactful.

Moreover, the economic impact of PPP loans extends beyond immediate relief. By supporting businesses through the pandemic, the program laid the groundwork for a more resilient economic recovery. As businesses rebuild and adapt to new market conditions, the support provided by PPP loans will continue to play a critical role in their long-term success.

Case Studies of PPP Loan Recipients

Case studies of PPP loan recipients provide a human perspective on the program's impact, illustrating the diverse ways in which businesses utilized their loans and the challenges they faced in the process.

Consider the story of a small family-owned restaurant in a rural community. Faced with declining revenue due to pandemic-related restrictions, the restaurant applied for a PPP loan to cover payroll costs and keep its doors open. The loan allowed the business to retain its staff, adapt its operations for takeout and delivery, and ultimately survive the economic downturn.

In contrast, a larger manufacturing company used its PPP loan to retool its production line and manufacture essential medical supplies. By pivoting its operations, the company not only preserved jobs but also contributed to the broader public health response.

These case studies highlight the adaptability and resilience of businesses in the face of adversity. They also underscore the varied applications of PPP loans, demonstrating the program's flexibility in meeting the unique needs of different industries and sectors.

Legal and Ethical Considerations

The PPP loan list of names raises important legal and ethical considerations, particularly in terms of compliance, accountability, and the responsible use of public funds.

Legally, businesses that received PPP loans were required to adhere to specific terms and conditions, including using the funds for eligible expenses and maintaining workforce levels. Failure to comply with these requirements could result in penalties, including the necessity to repay the loan in full.

Ethically, businesses faced scrutiny over their decision to accept PPP loans, especially if they possessed significant financial reserves or alternative funding sources. This raised questions about the moral responsibility of businesses to act in the best interests of their employees and the community.

The SBA and other regulatory bodies established frameworks to address these considerations, including auditing processes and public reporting mechanisms. These measures aimed to ensure that the program operated with integrity and that businesses were held accountable for their actions.

Loan Forgiveness Process

The loan forgiveness process is a critical component of the PPP, providing businesses with the opportunity to have their loans converted to grants if they meet specific criteria. This section will outline the steps involved in securing loan forgiveness and the challenges businesses may encounter.

To qualify for loan forgiveness, businesses must demonstrate that they used the funds for eligible expenses, such as payroll costs, rent, and utilities. Additionally, they must maintain employee headcount and compensation levels to the extent possible.

The forgiveness process involves submitting a forgiveness application to the lender, along with documentation supporting the use of funds and compliance with program guidelines. Lenders review the applications and make recommendations to the SBA, which has the final authority to approve or deny forgiveness requests.

While the process is designed to be straightforward, businesses may encounter challenges in navigating the requirements and gathering the necessary documentation. To assist with this, the SBA provides resources and guidance to help businesses understand the forgiveness process and maximize their chances of success.

Future of Small Business Loans

The lessons learned from the PPP and the insights gained from the loan list will shape the future of small business loans and government aid programs. This section will explore potential developments and innovations in this area.

One potential development is the increased emphasis on targeted aid, ensuring that future programs prioritize underserved communities and industries. This could involve new criteria for eligibility or the introduction of incentives to encourage equitable lending practices.

Another area of focus is the integration of technology in the lending process. Digital platforms and data analytics could streamline applications, improve transparency, and enhance the overall efficiency of aid distribution.

Ultimately, the future of small business loans will be guided by a commitment to supporting economic resilience and fostering a more inclusive and equitable business environment.

Frequently Asked Questions

- What is the PPP loan list of names?

The PPP loan list of names is a publicly available record of businesses that received loans under the Paycheck Protection Program. It includes details such as business names, loan amounts, and the number of jobs supported.

- Why was the PPP loan list made public?

The list was made public to promote transparency and accountability in the distribution of federal funds. It allows stakeholders to analyze trends and ensure that the program operated with integrity.

- How can businesses correct errors on the PPP loan list?

Businesses can report errors or discrepancies on the PPP loan list to the Small Business Administration. The SBA provides mechanisms for businesses to update or correct their information.

- What are the criteria for PPP loan forgiveness?

To qualify for loan forgiveness, businesses must use the funds for eligible expenses and maintain employee headcount and compensation levels. Documentation supporting compliance with these criteria is required for the forgiveness application.

- How did the PPP benefit small businesses?

The PPP provided financial support to small businesses, helping them cover payroll costs and operational expenses during the pandemic. This support helped prevent layoffs and business closures, contributing to economic stability.

- What are the future implications of the PPP loan list?

The PPP loan list offers valuable insights into the program's impact, informing future policy decisions and aid programs. It highlights the need for transparency, accountability, and equitable distribution of resources in government initiatives.

Conclusion

The PPP loan list of names is a critical resource in understanding the distribution and impact of the Paycheck Protection Program. By providing transparency and accountability, the list sheds light on the businesses that received support and the broader economic implications of the program. Despite controversies and challenges, the PPP played a pivotal role in stabilizing the economy and supporting businesses during a period of unprecedented uncertainty.

As we look to the future, the insights gained from the PPP loan list will inform the development of more effective and equitable aid programs. By prioritizing transparency, accountability, and inclusivity, future initiatives can build on the successes of the PPP and address the challenges that emerged. Ultimately, the legacy of the PPP and its loan list will continue to shape the landscape of small business support for years to come.

For further information, you may visit the U.S. Small Business Administration's official page on the Paycheck Protection Program.

Fraud Fallout From PPP Loans. It’s Getting Bad. Frank on Fraud

Ppp Loan List Of Names MarcusCathcart